Patriot Post: Social Security, Medicaid Rapidly Nearing Collapse

The Bitter Truth about Feminism

July 11, 2018

More Americans are Living Together and Having Babies Before They Get Married

July 11, 2018

Several recent reports combine to paint a frightening picture for America’s economic future if corrective action is not taken swiftly.

Patriot Post,

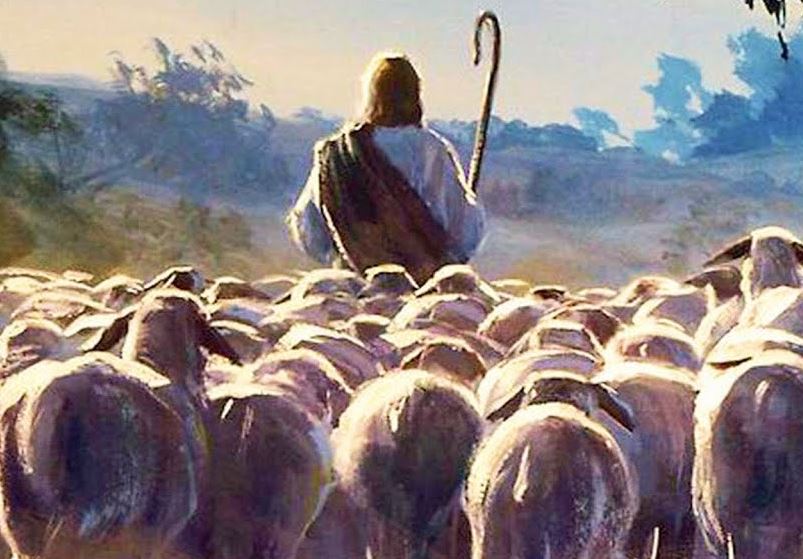

For years, fiscal conservatives have warned of the ticking time bombs1 that are America’s entitlement programs and were rewarded with mockery and contempt, dismissed as “The Boy Who Cried Wolf.” Unfortunately, as readers of Aesop’s fables recall, in the end the wolf actually existed, and it devoured the sheep.

Several recent reports combine to paint a frightening picture for America’s economic future if corrective action is not taken swiftly.

The first is a recent report by the Social Security Board of Trustees. It reveals that for the first time since 1982, the program must dip into its trust fund to pay benefits because the fund is now running a $200 billion annual deficit even as the number of beneficiaries (60 million and rising, with an average of 10,000 Baby Boomers a day retiring through 2029) continues to skyrocket.

This skyrocketing increase in beneficiaries is occurring at a time when Americans are having fewer children, or none at all (a staggering 60 million children have been aborted since Roe v. Wade, equivalent to killing the entire populations of New York, Pennsylvania, Maryland, Ohio and Georgia). These are children who will never live to enter the workforce or have families.

When FDR established Social Security, there were 42 workers for every beneficiary. Today that ratio is 3:1 and quickly approaching 2:1. There are simply not enough workers to fund the full benefits for 60-80 million retirees.

Even worse, bankruptcy is even nearer than we thought. According to a team of researchers from Harvard and Dartmouth, the Social Security Trustees have been using antiquated accounting methods (which they describe as “steering by sextant and dead reckoning” rather than using “global-positioning-systems”) and outdated demographic information to paint a rosier picture of Social Security’s future than is warranted. Updated projections from the Trustees report that the program will be insolvent within 16 years, but with their outdated accounting methods, insolvency is likely to occur within the next 10 years.

Politicians talk of a Social Security “trust fund,” but as the Washington Examiner’s Philip Klein notes, the trust fund is “an accounting fiction that pretends that spending doesn’t ultimately all come from the bank accounts of taxpayers.” He further notes that, with politicians borrowing from it for decades to cover general budget expenditures, the “trust fund” is nothing more than $3 trillion in IOUs, meaning the money is gone unless we raise taxes on current workers to repay the IOUs.

This is nothing more than “generational theft”2. We must either slash benefits to current retirees by 25% or more, or raise payroll taxes significantly on current workers, placing a tremendous burden on working families.

Up through 2010, retirees received more in benefits than they paid in contributions. That year, a couple received about $20,000 less than they paid in, and that ratio is getting worse each year. That is compounded by the fact that inflation drains even more from retirement accounts. According to a new study, Social Security benefits, due to rising costs and inflation, provide 34% less purchasing power3 than just 18 years ago.

Clearly, the answer is private retirement accounts, which not only accrue wealth far greater than Social Security benefits (which are now losing money for retirees), with even modest returns on investment “allow[ing] middle-income earners to retire on six-figure incomes,” but unlike Social Security, there are property rights in private accounts.

Americans would be shocked and outraged to discover that the Supreme Court has twice ruled that there is no right to Social Security benefits, regardless of how long or how much has been paid into the system. In Helvering v. Davis (1937), the Supreme Court upheld the constitutionality of Social Security, agreeing with Asst. AG Robert Jackson’s argument: “There is no contract created by which any person becomes entitled… [to] a claim for any particular sum of money. Not only is there no contract implied but it is expressly negatived, because it is provided in the act, section 1104, that it may be repealed, altered, or amended in any of its provisions at any time.”

The Supreme Court further expanded that ruling in Flemming v. Nestor(1960), concurring with the government’s argument that a beneficiary acquires no property right to benefits, stating that the claim that Social Security benefits are “fully accrued property rights” is “wholly erroneous.” For those who still doubt that Congress can reduce or even eliminate benefits at any time, the Social Security Administration states it right there on its website4.

So, barring a rare display of political bravery, which President George W. Bush and Speaker Paul Ryan were politically crucified for attempting with partial privatization, Congress will kick the can down the road until the house of cards collapses. Social Security is nothing more than a Ponzi scheme5, legal only because it is run by the government and more despicable because government forces us to participate in the fraud.

The situation with Social Security is bad enough, but Medicaid is even worse, projected to be insolvent in just eight years. Couple this with a $20 trillion national debt, rising federal spending and an estimated $91 trillion in unfunded entitlement liabilities6, and the situation is dire.

The time to act is now, before the wolf eats us.

https://patriotpost.us/articles/57028-social-security-medicaid-rapidly-nearing-collapse

Related posts

April 23, 2024

April 23, 2024

{kind=link}

April 23, 2024